|

|

Derivatives

and Risk Management

Power Marketing: By Scott Spiewak

Introduction Power marketing is a function which is novel for the electric industry. However, it is by no means a novel function. In every commodity market, marketing is used to meet customers’ demands. While the Federal Energy Regulatory Commission ("FERC") certifies "power marketers," this is merely a regulatory definition, and not a commercial one. Traditional utilities, as well as the new nonutility marketers will necessarily engage in marketing in the service of their customers. Power marketing is price creation through the use of price risk management tools. The purpose of this monograph is to provide an introduction to those price risk management tools, known as "derivative" products, and their application.

Background Almost since its inception, electric service has been treated as a monopoly. This meant that the entities which sell electricity have been required to do so on a cost of service basis. Rates were regulated, and based upon cost of production. There was no price differentiation. This began to change with the implementation of PURPA, as for the first time, certain qualifying power companies could sell their output without having their costs subjected to regulatory scrutiny. A "rate" was set, based upon the purchasing utility’s avoided costs, and the qualifying power company would garner profits (or losses) based on how well it could control its own costs. While this was in itself revolutionary, it was well short of true price creation. However, it did start the process moving. By the latter part of the ‘80s, the concept of avoided costs had been largely displaced by competitive procurements run by utilities seeking low-cost power supplies. The purchaser’s costs were to be measured by the market alternatives. With this step, a crude market was created. However, this nascent market was still constrained by the limited ability of purchasing utilities to seek suppliers beyond their immediate neighbors. There were only limited rights to transmit power over those neighbors’ lines. By the early ‘90s, it had become clear that the industry and the nation would benefit if low-cost electricity could flow more easily. Congress responded by passing the Energy Policy Act of 1992 (EPAct). EPAct granted the FERC the authority to require utilities under its jurisdiction to transmit power. Over a period of years, FERC issued a series of orders and policy statements implementing EPAct. This process culminated with FERC’s Order 888 which finally required utilities to file "pro forma" transmission tariffs—standard transmission contracts available to anyone in the wholesale market. With FERC Order 888 in place, a true wholesale market has developed. Power is now regularly traded over distances not previously feasible, increasing the efficiency of the electric industry by permitting higher-cost generation to be displaced by lower-cost resources. Markets have expanded and become more efficient. But this physical change was just the beginning. The ability to move electricity provides physical liquidity. The next step, quickly recognized, was to create price transparency—the ability to quickly and accurately determine the price of electricity. In a regulated industry, there are no prices, just cost-based tariffs. As we continue to shift to a market model in the electric power industry, prices become all-important. It is the means by which consumers select their suppliers. The first steps in achieving price transparency are taking place—

Electricity is now well on its way to becoming commoditized in the wholesale market. This price transparency in the wholesale market has been noted at the state level, where utilities, commissions and legislators are increasingly looking to follow FERC’s lead, encouraging competition at the retail level. California, New Hampshire, Rhode Island, and Pennsylvania have passed laws permitting customers to choose alternative power suppliers. Utilities in Illinois, New York, Massachusetts, New Hampshire, Washington and Idaho have implemented pilot programs and are currently allowing retail customers to select the suppliers of their choice. When given that choice, customers select their suppliers, overwhelmingly, based upon one thing—price. However, prices don’t appear out of nowhere. They are created. Price creation is the key element of power marketing. The implications of this for the electric power industry are dramatic. As electric power becomes deregulated, it will begin to act more and more like other energy commodities. Marketing of energy commodities is engaged in by energy producers in other industries, and traditional power generation companies will employ the tools of marketing also. However, they will be joined by other commodities traders—oil and natural gas trading companies, Wall Street trading firms and commodity investment houses. In the commoditized energy markets, most transactions are not between producer and consumer, but among marketers, continuously building and adjusting their portfolios in order to deliver a competitive price to their customers. Electricity is merely the last of the great regulated industries to be subjected to deregulation and commoditization. As this process continues, we are already seeing the new products which will change the nature of the industry. These products are what are known as derivative products. Derivative products are the bulwark of a global price risk management system. The following pages explain how derivatives can be used in energy commodity transactions.

Power Marketing: The prices in the cash trading market and the physical commodity market converge over time. During this time derivatives can be used to manage the risk of price volatility. The basic derivative products are:

Forward Contracts. A forward contract is an agreement for the delivery of a commodity in the future, generally for a term which may be from a month to years long, at prices fixed at the inception of the agreement. Forwards do not trade on exchanges and therefore offer more flexibility to contracting parties but more risk than exchange traded derivative instruments. While the electric power industry has long had multiyear agreements, these have been primarily cost-based agreements, in which the price was not fixed, but rather fluctuated with the suppliers’ cost of production. Because prices were not fixed at the inception of the agreement, these multiyear contracts cannot be considered forward contracts. Forward contracts have been uncommon outside the realm of PURPA-mandated, long-term contracts based upon projected avoided costs. To the extent that these contracts were the product of regulatory mandate, they are poor examples of true, market-oriented forward contracts. Nevertheless, the forward contract is the bulwark of the marketers’ business. When a customer needs power supplies, it goes out for bid. The key component of a winning bid is a fixed price for the term sought. It is impossible to win or hold customers in a competitive market without the capability to offer forward contracts. Fixed price forward contracts will need to be created, in volume, on demand, and in a fashion which permits the supplier to "lock in" a certain price. In their crudest incarnation, forward contracts may be offered directly by a marketer which simply relies upon its own views of the future, as reflected in its internal "forward curve," and which is willing to bet that the price it offers in the forward contract will be above its cost of production or acquisition. However, this is a risky way to do business. The market is punishing toward a marketer which offers "unhedged" forward contracts. If it turns out the costs are higher-than-expected, the marketer can lose tremendous amounts of money quickly. For example, if a marketer were to agree to deliver 200,000 mWh over a one year period at a fixed price of $20/mWh, and the actual cost of obtaining and delivering power was $30/mWh, the marketer could lose $2 million on that single transaction. In order to protect against these losses, in the absence of hedging mechanisms, the marketer will only offer to sell forward contracts at relatively high prices, and to buy under forward contracts at relatively low prices, creating a large "spread" between purchase and sale prices. The larger the spread, the less efficient the market, and the more customers must pay for a priced product. To improve market efficiency, marketers have supported the New York Mercantile Exchange (NYMEX) in its efforts to establish electricity futures contracts. Two of these are already trading.

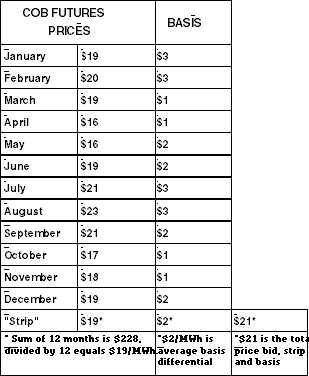

Electricity Futures. A futures contract is a standardized contract, traded on an exchange, and subject to regulation by the Commodities Futures Trading Commission (CFTC). Futures’ standardization provides more financial liquidity than other devices in the world of commodities. There are currently two NYMEX electricity futures contracts. The difference between the two contracts are their delivery locations. One contract is for delivery at the California-Oregon Border, which is referred to as "COB," and the other is the Palo Verde substation in Arizona. Otherwise, the terms and conditions of the contracts do not differ. The electricity futures contracts require the seller of a contract to commit to deliver 736mWh each month at the contract price agreed to. The contracts are for firm energy. This number comes from the requirement that electricity be delivered in increments of 2 mW per hour, for 16 hours each business day, beginning at 6 a.m. and ending at 10 p.m., 23 business days each month (there are provisions for delivery on certain Saturdays during short months). 2 x 16 x 23=736. This obligation to deliver is backed by the exchange (NYMEX). Futures’ contracts cannot be negotiated, except for price, which once set, is locked in for the month covered by the contract. The fact that the contracts are standard is what makes them liquid, and therefore valuable for power marketing purposes. Contracts are traded out eighteen months, which makes them more than adequate for the creation of the most popular futures contract, the fixed price, one year contract. To understand the importance of the futures contract to marketers, compare the situation of a marketer facing a California customer in 1998 with and without the NYMEX futures contract. Without the futures contract, the marketer must guess what the cost of electricity will be during 1998, then build in a hedge to protect against errors. With futures contracts, marketer risk can be substantially controlled, by purchasing a "strip" of futures contracts—that is, one futures contract for each month of the year-long customer forward contract. When the customer asks for a price quote, the marketer simply checks to see the current offered price for futures contracts for the twelve months, calculates a weighted average, and makes an offer to the customer. If the customer accepts, the marketer purchases the strip, and to a great extent, locks in its profits. The guesswork of creating a forward price offer is largely eliminated, dramatically reducing the spreads required by the marketer, and thus reducing the price paid by the customer.

Creating a forward price offer using futures contracts

In this example, the customer may be offered a price of just above $19/mWh for peak hours. How far above depends upon the marketer’s overhead and profit requirements for the transaction. It is important to note that while the purchaser of a futures contract can take delivery of its electricity at the trading hub, almost none do so. Over 95% of these contracts are "closed out" before it is time for them to go to "delivery." This is accomplished by simply selling one futures contract for every contract purchased. Why do this? Because the primary purpose for futures contracts is to act as a financial hedge, not as a source of electricity. In the example above, a marketer purchases a futures contract for August delivery at $23/mWh. The summer turns into a hot one, and electricity prices soar to $33/mWh by the end of July. The purchaser simply sells the contract for $33/mWh, taking a $7,360 profit (736 MWHs per contract x $10 per MWH profit). This profit is then used to offset the cost of purchasing physical power in August. The purchaser could take delivery at the California-Oregon Border, and transport the power to where it is needed, say in Southern California. However, there may be local powerplants which can sell electricity for less than the COB price-plus transportation costs. It is therefore generally more efficient to rely on the futures market for the financial hedge, while obtaining physical electricity supplies elsewhere. The exchange-traded futures contracts are extremely important for marketers, and will be traded in massive volumes as customers are offered fixed price forward contracts. To understand just how large this business will become, it is useful to compare the natural gas industry to the natural gas futures contract. The U.S. uses $60 billion in natural gas (retail) each year. To provide fixed prices just to that segment of the market which can access them, and which are not still exclusively served by local distribution companies, gas marketers purchase $300 billion worth of natural gas futures each year. The dollar volume of the natural gas futures contract exceeds the actual physical volume consumed by 500%, and the natural gas market is only about 50% deregulated! If electricity follows the same pattern, as is likely, we can expect the $200 billion electricity industry to be supported by a trillion dollars in futures contract trading within the next five years, as retail markets open and customers demand price quotes. To help this occur, NYMEX is planning additional futures contracts. It is anticipated that by the summer of 1997, NYMEX will launch at least one more electricity futures contract in the eastern interconnection, to supplement the two currently traded in the western interconnection. This is necessary, because the eastern and western interconnections can physically tolerate little trade between them, and prices between the two interconnections therefore have little in common. In fact, this problem of requiring separate trading hubs in the east and west mirrors a similar problem within each synchronous region. There are lesser, but still serious, transmission constraints within regions which make it likely that prices in one subregion will differ from those in other subregions. Theoretically, NYMEX could create dozens of futures contracts. However, it must balance the need for comprehensive coverage against the loss of liquidity which would result from a proliferation of futures contracts. If there are too many futures contracts, it becomes less likely that a marketer will be able to buy and sell any particular contract on demand. Thus, NYMEX must limit the number of trading hubs for which it provides futures contracts, and leave the remaining risks to off-exchange mechanisms—the so-called "over-the-counter" products. Of primary importance among these over-the-counter products is the "basis contract."

Basis Contracts. Basis contracts reflect, and are designed to permit marketers to hedge against fluctuations in the difference in prices between two location points. Typically, one point is a NYMEX futures contract trading point, such as COB, with the other point being a heavily-traded subregion, for example, Sacramento. When a customer in Sacramento requests a price quote for a one-year forward contract, the marketer can readily calculate a strip of NYMEX contracts traded at COB, and make a price offer. Most of the risk in making that offer can be eliminated, by simply "buying the strip." However, the marketer still has to deliver power to the customer. One way of doing this would be to simply purchase firm transmission from the California-Oregon Border (COB) to Sacramento for the year term. The marketer can look up the tariff, add in the firm transportation price to its bid, and be done. However, such a marketer will regularly be undercut by other, more competent marketers. This is because it may be possible to purchase power locally, and avoid transportation costs. This may be done all year long, or just part of the year. It might be done on a full requirements contract, or as a standby contract so that the marketer can use interruptible transmission. There are numerous approaches which may be used to assure that the Sacramento customer gets its power supply without the need to physically transport power from COB. But most marketers will never deal with this. Rather, they will rely on market makers in basis—marketers which specialize in "basis contracts," who will guarantee a price differential between the NYMEX contract and a subregional trading point such as Sacramento. There are even circumstances in which a basis contract can be a negative number. Thus, for example, because electricity can be less expensive in Alberta than at the California-Oregon Border, it is not unusual for a basis quote to be "COB minus" for power delivered to Alberta. Basis contracts are generally less expensive than purchasing year-round firm transportation, which is why a marketer must use them in order to survive in a competitive environment. The marketer which specializes in basis contracts for a given region makes its money by estimating correctly the price difference between one point and another. It studies transportation tariffs, but also nonfirm transmission rates, numbers of interruptions of nonfirm transmission service on various routes, and the cost of purchasing electricity at secondary trading points. This type of calculation is qualitatively the same as that made by the marketer offering forward contracts in the absence of the NYMEX futures contracts. However, because the NYMEX contract eliminates the greatest share of the risk, basis risk is quantitatively much smaller. In sum, basis contracts permit the marketer to lock in differences in prices between two points, typically a NYMEX trading hub and a secondary trading point. Just as NYMEX prices fluctuate continuously, so, to a lesser extent, do basis quotes. Also, just like NYMEX prices, basis prices will differ month-to-month (although generally price quotes for basis contracts will be the same for months during the same season). In the example here, basis prices have been added to a "strip" to bring the marketer closer to the final price quote to be given the customer.

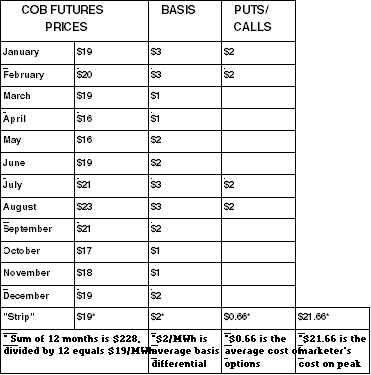

Options Contracts. Now the marketer has in place a NYMEX strip, and a basis contract. He can make an offer to the customer of a fixed price contract for the year, and rest easy, knowing that if accepted, he has locked in his profit. But has he? Customers, particularly smaller customers, demand "full requirements contracts." These are contracts in which the customer pays the same price per kWh, no matter how many kWhs they use. Experience has shown that customers are willing to accept the idea that if they buy more electricity, they have to pay more—but customers don’t want to be told that their price will change. After all, they selected their supplier based upon price. In the example above, the customer has a flat load factor—i.e., it uses the same amount of electricity in each month. This is not often the case, but different load factors do not present a difficult problem for the marketer. A typical customer will use more electricity in the summer than in the spring or fall. To compensate, the marketer may buy two futures contracts for July and August, when the air conditioning is on, for every one futures contract it buys for April and May, when the windows are open. Then the "strip" becomes a weighted average of the contracts required to be purchased for the customer. A customer which uses a great deal of electricity during summer peaks will pay more per kWh than a customer which uses electricity in constant quantities. However, this leaves the supplier with another problem. It has made an offer based upon the customer’s projected pattern of use, often based upon historical averages. But what if it is an exceptionally hot summer? Or, just as problematic, what if it is an exceptionally cool summer? In the first case, the marketer won’t have locked in the price on sufficient power supplies, and may have to buy on the open market at high prices. In the second case, the marketer may have too much power supply locked in, and it may have to sell in a depressed market. A marketer, operating on thin margins, can afford neither. To protect against these possibilities, the marketer may use options contracts. These come in two basic types: calls and puts.

Call Options The purchase of a call option gives the buyer the right, but not the obligation, to purchase the commodity at a set price. One can purchase a call option on an electricity futures contract. If, for example, electricity contracts are trading at $20/mWh for July, one might purchase the right to buy that contract for perhaps $1/mWh. This would effectively "cap" the price of additional July power at $21/mWh (the option price plus the exercise price). However, should July be a normal month, and the marketer didn’t need the power, it would be under no obligation to take it. The marketer would simply choose not to exercise its "call option."Thus, call options permit the marketer to offer a "full requirements contract," at a fixed price, with minimal risk that the marketer will lose money by having to purchase high-priced power in a hot summer.

Put Options Similarly, there is a risk that July will be unusually cool. In such cases, customers will not use as much electricity as was projected, and electricity prices are likely to fall. The marketer would have to sell its surplus electricity at a loss, unless it has "put options." A put option gives the holder the right, but not the obligation, to sell electricity at a predetermined price. To extend our example, the marketer might purchase a put option with a strike price of $20/mWh, for a cost of $1/mWh. If prices fall, the marketer can exercise its put option, and sell the electricity for $20. If a marketer uses options, it is only likely to use them during periods when unusual weather would have a severe impact — i.e., during summer and winter peak periods. The cost of the call and put options can be included in the price bid to the customer. The marketer now has a basis for making a price offer to the customer. It will be $21.66 plus an amount designed to cover the marketer’s overhead, profit and risks, including accounts receivable risk, and residual price risk. Puts and calls on electricity futures contracts are themselves traded on the NYMEX. However, options may be purchased on other products, such as basis contracts, also. These are not exchange traded, and therefore are referred to as "over-the-counter options." Also, some marketers won’t bother with options, but will rather take the risk themselves, effectively managing this residual risk internally. Options are powerful tools, and may be used for a variety for hedging and speculative purposes by more sophisticated marketers. For example, a power producer might purchase a "put" in order to place a floor under its revenues. By purchasing a put with a "strike price" of $20/mWh, a power producer guarantees that it will receive at least $20/mWh. If market prices are higher, the power producer simply chooses not to exercise the put, and sells at market rates. If market rates are lower, the producer exercises the put, and sells at the $20 floor price. A power producer could also obtain additional income by selling a "call." By selling another company the right, but not the obligation, to buy power at $25/mWh, the power producer earns premiums—the amount paid by the buyer of the call option. However, the price it pays is that if market prices go above $25/mWh, the purchaser of the call will surely exercise it, and force the producer to sell at a ceiling price of $25/mWh. The power producer can even combine the two. By simultaneously purchasing a put and selling a call, a power producer can create what is known as a "no-cost collar," in which the price of electricity can go no lower than the floor created by the put, and no higher than the ceiling created by the call. The premium payment received in return for the sale of the call offsets the premium payment made to purchase the put. Futures contracts, basis contracts, puts and calls on futures contracts are the most commonly used derivative products. The customer seeking the most common product, a fixed price, can almost be satisfied by the marketer utilizing these tools. However, the NYMEX only offers futures contracts for electricity used during peak periods. Until it begins offering futures contracts covering off-peak usage, marketers must use yet another financial tool—the electric rate swap.

Electric Rate Swaps. NYMEX has chosen to implement futures contracts only for on-peak periods—those 736 business hours each month, or 4416 hours in a year during which prices are the most volatile. But this is only about half the hours in a year, and customers want power 24 hours a day, 365 days each year. Customers require that the marketer deliver power during the off-peak periods, and to similarly guarantee a price to the customer for those off-peak hours. Off-peak power is by definition less expensive than on-peak power, and it generally has less price volatility. However, the price risk associated with off-peak power is still significant. In some regions, it is not unusual for market indices to list ranges of over $5/mWh for off-peak power. This is far greater than the typical profit margin on those sales. Therefore the prudent marketer must hedge the risks associated with those price swings. This is accomplished by means of what is called an "electric rate swap," and specifically, a "plain vanilla swap." In a plain vanilla swap, the marketer exchanges a fluctuating rate, typically a market rate, for a fixed rate. Contracts calling for market rates often cite a commonly-accepted electricity market index, such as the Dow Jones’ Telerate indices or McGraw-Hill’s Power Markets Week indices. They are also traded at common delivery points, such as at the "citygate1" of utilities with large numbers of customers which might be available for marketers to serve. In order to complete the construction of the customers’ price, the marketer must obtain a "swap" to lock in the price of off-peak power to the customer, typically at the citygate of the utility serving the customer. A swap which is not done to the citygate might require the marketer to get yet another basis contract for off-peak power, or to simply estimate and absorb the risk associated with swings in transmission prices during off-peak periods. For our purposes, we are assuming a swap to the citygate. Swaps are available from swap market makers. These may be power marketers, or even financial institutions. As will be described below, swaps are the purest of financial transactions, with no possibility of physical electric delivery. When added to the other products used to produce a price for electricity to the customer, the final calculation looks like this: The marketer now has a cost of purchasing commodity to supply its customer—$17.83/mWh. To this it adds a figure to cover its overhead, including residual price risks, and acounts receivable risks, an additional figure to cover its profit, and without further ado, it can make a price offer.

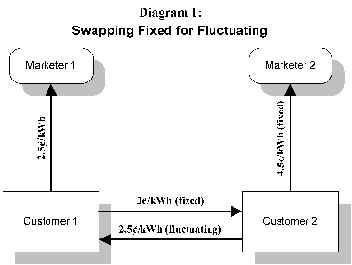

Understanding Swaps Electricity price swaps, while playing only a minor role in our story thus far, are the most flexible of financial tools, and may be used to create a variety of innovatively priced products. Swaps are traditionally described using a device known as a "swap diagram." To understand the swap diagram, it is important to remember that what we are describing is the flow of money, and not the flow of electricity. Diagram 1 is a description of our simple plain vanilla swap, of the type used to complete our simple fixed price transaction.

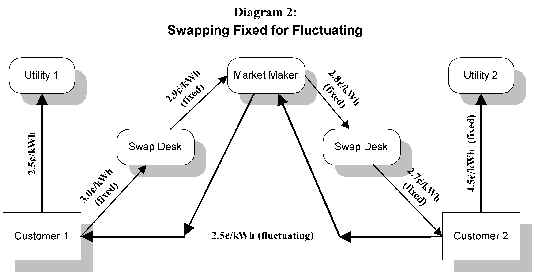

In the diagram and accompanying table, Customer 1 (C1) starts out paying Marketer 1 a "fluctuating rate," which averages 2.5�/kWh. Customer 1’s problem is that it needs to set a budget, and protect itself against market fluctuations. To do this, it needs to identify a counterparty which is willing to take the market risk, in return for a fixed payment stream. The fixed payment stream is generally higher than the projected payment stream, based upon historical usage, to take into account the risk C2 is taking on. C2 is willing to take the risk, because it expects to come out ahead in the end (although there is no guarantee that it will). CI, on the other hand, doesn’t expect to come out ahead—it is merely buying insurance against extreme price fluctuations. Because this is a pure financial transaction, Marketer 1 need not even be aware it is taking place. C2 simply pays C1 an amount equal to its electric bill. In return, C1 pays C2 three cents per kWh. The ultimate result is that the 2.5� (average) payment to Marketer 1 is cancelled out by C2’s payment, leaving C1 with a 3�/kWh fixed payment to C2. C1 has accomplished its goal of rate stabilization. C2 has the goal of getting an immediate rate reduction, with the possibility of future rate reductions should the cost of generating power fall. It accomplishes this by enticing C1 to pay it a premium rate in return for rate certainty—C1 pays 3�, reducing C2’s fixed costs to only 1.5�/kWh. Of course, C2 has to pay C1’s variable-rate electric bill, but that is only 2.5� currently. Add the 1.5� fixed payment and the 2.5� variable payment and C2 is still only subject to a current charge of 4�/kWh. C2 has an immediate savings of .5�/kWh, and the possibility of additional savings should the cost of power from Marketer 1 fall in the future. In order to accomplish this transaction, the counterparties need to be comfortable with each others’ financial situation. If one party goes bankrupt during the term of a swap, the other won’t get the benefit of its bargain. This is what is known as counterparty risk. In addition, it is extremely difficult to find counterparties with precisely counter-vailing risk profiles. For example, it is unlikely that both C1 and C2 use precisely the same amount of electricity. This means there will be unhedged leftovers, or nubs on the transaction. The development of price indices creates the conditions for solving most of these problems. By standardizing the fluctuating measure, price indices have permitted there to be created a market in price swaps. Rather than identifying a counterparty for each transaction, familiarizing each with the credit risks of the other, and dealing with transaction nubs, customers can deal with market-makers. Market makers establish prices for swapping the index, and handle many transactions, quickly and cheaply. Today, it is rare for counterparties to deal with each other directly. It is far more efficient to work through the market makers. The market for swaps is therefore coming to look more like this:

Freedom to Focus on Core Competencies Rather than the one-on-one transactions we have had to do in the past several years, market-makers make it possible to do many transactions without perfect matches among customers. This vast increase in liquidity is permitting new rate products to be created which allow companies to focus on their core competencies, such as running powerplants well.

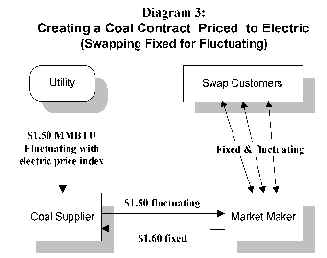

Example 1: Coal priced to electricity For example, many utilities are moving away from long-term fixed price coal supply contracts. These contracts have often resulted in power costs which are "out-of-the-market," even though the powerplant is running well. An ideal solution to this problem is a coal supply contract which is price-indexed to electricity. That way, if electric prices fall, coal prices fall. If electric prices rise, coal prices rise. In either case, so long as the plant is run well, the power company will continue to make a profit. Without electric price indices, it is very difficult (and expensive) for a coal company to offer coal at prices marked to electricity. One has to establish what the measure is and gain confidence that it can’t be manipulated. With an electric price index in place, it is a relatively simple matter to offer coal at electricity-based prices. The transaction looks like this (arrows show direction of money):

The Utility pays the Coal Supplier a rate which fluctuates with an electric price index. The Coal Supplier, needing a fixed payment stream to cover its largely fixed mining costs, "swaps" that "fluctuating" payment stream for a "fixed" payment stream through a price swap market-maker. The market- maker is continually swapping fixed for fluctuating based upon the index, and so can readily name a price for doing the swap.

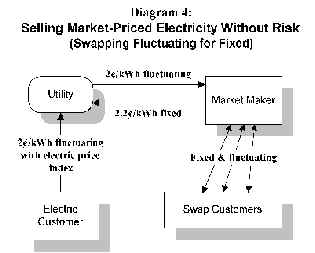

Example 2: Selling electricity at market rates without risk Increasingly, electric power customers are seeking electric suppliers which are willing to sell at the "market price." Indices provide not only the basis for determining that market price, but a means of hedging the risk associated with such an offer. The customer wants market-based rates. The power company needs to cover the fixed costs associated with power production. These wants and needs can be reconciled through the use of price indices:

In this case the Utility receives a "fluctuating" payment stream from the customer, based upon the "market price" of electricity. But because that market price is based on an index, it can be easily "swapped" for a fixed rate with a market-maker. Electric rate swaps can also be used to create "exotic" specialized electric rates, such as electric rates which fluctuate with aluminum prices, steel prices or natural gas prices. These are useful for customers which see their profits, and their ability to pay for electricity, closely linked to the price of another commodity. These cross commodity swaps can be extremely attractive to large specialized industrial customers.

POWER MARKETING: THE KEY CUSTOMER SERVICE FOR A COMPETITIVE MARKET The purpose of this treatise is to explain the fundamental principals and products used in power marketing. As in other commodity industries, customers will select their electric power suppliers based primarily upon price. Power marketing creates prices to offer to potential customers. Prices make things simple for the customer, yet creating them makes business much more complicated for suppliers. Customers generally don’t want to hear about the difficulties of a supplier in arranging for futures contracts in a timely fashion, or about the illiquidity of basis trading for one of their locations. From the customer’s perspective, weather-related variations in usage should not result in price changes—that is a problem for the supplier, not for the customer—a marketing problem to be managed with marketing tools. The natural gas industry, the closest analog to the power industry, delivers $60 billion worth of gas to retail customers every year. It is supported by $300 billion in gas futures trading and another $300 billion in over-the-counter derivative products. That is, the wholesale market is ten times the size of the retail market. Virtually this entire market was created in the 1990’s. Presuming that electricity follows a similar course, in a few years the larger, $200 billion retail electricity market will be served by a two trillion dol1lar derivatives market, consisting half of electricity futures contract trades and half of options, swaps, forwards and basis trades. From this it should be clear why there are now over 250 nonutility power marketers registered to do business in the U.S. There is a great deal of work to be done—work which has little or nothing to do with the traditional functions of the electric power industry. The addition of power marketing to the power industry does not take anything away from existing power companies—this is not a zero sum game. Generation, transmission and distribution will continue. Power marketing is an entirely new function. It can be performed by traditional power companies, or by others, but it must be performed. Customers demand it.

Reprinted with permission, Scott Spiewak, The Power Marketing Association and The Edison Electric Institute. All rights reserved. Copyright 1997.

|

||||||

![]()